How to Increase Your Credit Score

From $10,000 in Debt to an 842 Score!

Like many young adults, I went a little crazy with credit cards when I was somewhere between 18-22. At that time, I was $10,000 in debt and felt like it was the biggest, most irresponsible thing I could have done with my financial life! Granted, wealth and debt are relative, but it was a heavy burden to bear at that age. I felt it was a big deal, so it was -- to me. I did a lot of research about what it takes to improve one's credit score. I never paid a company to do it for me. And I followed through consistently with what I learned. Many years later at a real estate investor’s association, I took an in-depth class on this topic from an executive at a large national bank . . . and I learned nothing new! This is how thorough my knowledge had become.

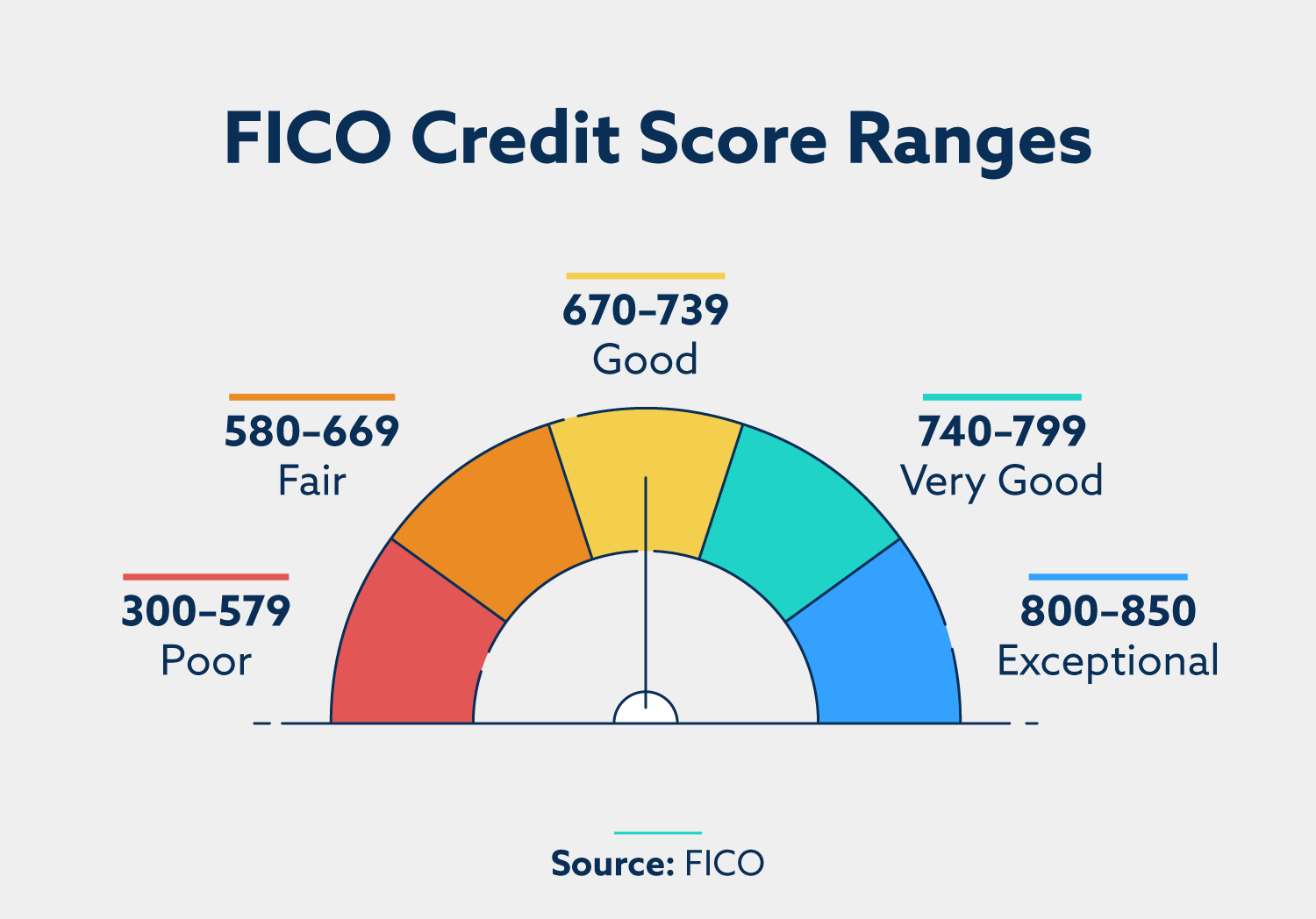

The following is based on my first-hand experience of having a low credit score (I don't recall the actual number, it's been too long) to 842 when I purchased a vehicle just a few years later. (The scale tops out at 850.) It didn't take that long to improve my score, but it wasn't overnight either. Look at this as a medium- to long-term play. Once you start seeing your score regularly climb higher and higher, you may get addicted to seeing it improve by the good choices you make every day! Then it gets easier to do. You may start thinking about the buying power you'll gain with your new higher score. You may realize that by getting a better interest rate as a result of your better score, you also increase your buying power, including buying a home or investment property. Woohoo! That's energizing! Let's dive in . . .

There are 6 major categories, most of which are in your control. Read on OR watch the video which contains the same information:

Most lenders use a FICO scoring model. While there are variations, the major factors still look like this:

Payment history – about 35%

Credit utilization – about 30%

Length of credit history – about 15%

Credit mix – about 10%

New credit and inquiries – about 10%

Most of these are fully within your control.

What Actually Impacts Your Credit Score in 2026

This simply means: how much of your available credit are you using? If you have one card with a $1,000 limit and charge $500, your utilization is 50%. That’s high. If you have two cards with $1,000 limits each and charge $500 total across both, your utilization is 25%. That’s much better. Generally, you want to stay under 30%. Lower is even better. Many high scorers stay under 10%.

Where people make mistakes: They close unused credit cards. When you close a card, you reduce your total available credit. That instantly increases your utilization ratio, even if your spending habits don’t change.

Now, here’s a nuance: closed accounts can remain on your report for years and still count toward your history during that time. But if your goal is to maximize your score, keeping older accounts open usually helps.

If a card has no annual fee and no risk issues, it often makes sense to keep it open and charge something small to it occasionally. Charge something, even a $5 coffee once every few months, to prevent the credit card company from closing it from lack of use. (This happened to me, and it dipped my score!)

Bonus Tip: After a long stretch of on-time payments, request a credit limit increase. Many issuers let you do this online. Do not increase your spending. The goal is to increase your credit limit to lower utilization, not higher debt.

1. Credit Card Utilization - High Impact

This is the big one. Pay every bill on time. Every time. Forever.

Even one 30-day late payment can drop a strong score significantly. Put accounts on auto-pay. Personally, I use the credit card company’s auto-pay system rather than relying on my bank’s bill pay. I’ve had a bank glitch before. I don’t take chances.

Let me clear up a myth I once heard in a class: “You need to leave a balance and pay interest so lenders know you’re using credit.” Not true! I have not paid interest on any credit cards in over 20 years. I pay my full statement balance every month. That is what matters. Paying in full still counts as responsible use. There is no secret scoring category that rewards you for paying interest.

2. Payment History - Highest Impact

3. Derogatory Marks - High Impact

These include late payments, collections, charge-offs, foreclosures, judgments, tax liens.

I once had a disreputable property management company try to charge me for normal wear and tear. I refused to pay it. They reported it.To my surprise, my score barely moved. Why? Because I had over a decade of perfect history and strong performance in every other category. Context matters. A single issue on an otherwise pristine file doesn’t carry the same weight as a pattern of problems.

If you have legitimate errors on your report, dispute them directly with the credit bureaus. You do not need to pay a company to do this. If a creditor cannot verify the debt, it must be removed.

If you truly owe the debt and cannot pay it in full, negotiating a settlement is sometimes better than allowing it to spiral into full collections. It may still impact your score, but less severely than prolonged delinquency. Also, ask the collector if they will remove the derogatory mark if you pay it off while on the phone. They may ask you simply pay X amount over what's due (yes, they'll pocket that extra and pay off the original creditor) and they’ll remove the derogatory mark. It doesn’t hurt to ask!

And remember: most negative items age off after about seven years. Time does heal credit.

4. Length of Credit History - Medium Impact

Lenders like to see that you can handle different types of credit responsibly. For example, credit cards, auto loans, mortgages, installment loans.

You don’t need to open loans just for the sake of “mix.” But over time, as life naturally includes these things, responsible handling strengthens your profile.

6. Hard Inquiries - Low Impact

There is no trick. There is no hack. There’s consistency.

Keep utilization low.

Pay everything on time.

Avoid unnecessary new debt.

Let time work for you.

Credit scoring is not emotional. It is mathematical. If you behave predictably and responsibly, the score eventually reflects that. When I went from stressed and in debt to an 842 score, it was not because I made more money overnight. I actually didn’t! It was because I changed my habits and understood the system. Higher credit doesn’t just feel good. It lowers interest rates. It increases buying power. It gives you options. And options are powerful.

Start today and stay consistent; your future self will thank you!

Written by Daisy Espeland, 1% Real Estate Broker in Central Florida

This includes:

Age of your oldest account

Average age of all accounts

The longer you demonstrate responsible behavior, the better. The is similar to auto insurance quotes – usually, the younger the driver, the riskier he or she is to insure. This is another reason not to close old accounts unnecessarily. Older accounts support your average age.

An account can be closed by the creditor without notification if you never use them for an extended period of time. Thus, periodically (say, once every 4 months) charge a little something on it. Or, to do this without thinking about it, always charge one household bill on it, such as your Internet bill. Just one will do. And always pay it in full. All of this can be done on auto-pay.

If you’re new to credit, be patient. You cannot rush time. But you can avoid resetting the clock by constantly opening and closing

5. Credit Mix - Low to Medium Impact

Many people are more concerned with this category than any other, when in reality, it has a low impact on your score. When you're starting out with credit repair though, be strict with every category until your score can handle any type of hit - even a low impact hit. When you apply for new credit, a hard inquiry is recorded. One inquiry typically has a small, temporary impact.

When shopping for a mortgage or auto loan, multiple inquiries within a short window are usually treated as a single inquiry for scoring purposes. That’s intentional. You are allowed to comparison shop. Just don’t apply for multiple credit cards impulsively within a short period if you’re actively trying to boost your score.

The Real Secret

A Modern Note: “Buy Now, Pay Later”

Some newer scoring models are beginning to incorporate Buy Now, Pay Later accounts if they are reported. Responsible use may help. Missed payments will absolutely hurt. Treat those agreements with the same seriousness as any other credit.